As we are heading into the holidays and the New Year, I have received several questions from current clients, prospective clients and other practitioners regarding the disclosure period for Offshore Voluntary Disclosure Program and Streamline filing compliance procedure.

What happens if the practitioner is working on a submission and fails to submit it before 12-31-14?

Does that mean that the practitioner has to wait until the 2014 tax return is filed in 2015 to submit the offshore or streamline filing?

What about the FBAR reports for 2014 that are due in June 2015? How does that play into the equation?

Finally, what about information filings such as 3520, 5471, 8865, etc?

In an effort to answer these questions and provide transparency, here is a general breakdown of the disclosure period timeline assuming filing requirements for all years:

1. Disclosure Period for Federal Individual Income Tax Returns (1040)

OVDP Prior to 04-15-15

OVDP After 04-15-15

Streamline Prior to 04-15-15

Streamline After 04-15-15

2006-2013

2007-2014

2011-2013

2012-2014

OVDP FAQ 9[1]

OVDP FAQ 9[2]

SDOP 1[3]

SDOP 1[4]

2. Disclosure Period for Report of Foreign Bank and Financial Accounts (FBAR)

OVDP Prior to 06-30-15

OVDP After 06-30-15

Streamline Prior to 06-30-15

Streamline After 06-30-15

2006-2013

2007-2014

2008-2013

2009-2014

OVDP FAQ 9

OVDP FAQ 9

SDOP 8[5]

SDOP 8[6]

3. Disclosure Period for Information Returns (e.g., Forms 3520, 3520-A, 5471, 5472, 8938, 926, and 8621).

OVDP Prior to 04-15-15

OVDP After 04-15-15

Streamline Prior to 04-15-15

Streamline After 04-15-15

2006-2013

2007-2014

2011-2013

2012-2014

OVDP FAQ 9

OVDP FAQ 9

SDOP 1

SDOP 1

IRS Forms

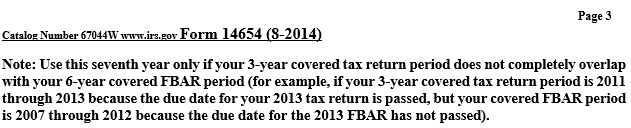

With an Offshore or Streamline disclosure, it is a good idea to always review the IRS submission forms thoroughly. In the past the forms were not very helpful, but through recent changes and suggestions from practitioners, the forms now have helpful directions. For example, there is liminal period that occurs between the 1040 filing deadline of 04-15 and the FBAR filing deadline of 06-30. During this period there may need to be additional information submitted for the disclosure

Example: See the top of page 3 of the Streamline Domestic Submission Form 14654:

Please note that this is not legal advice and should not be relied upon as such. Taxpayers should consult with a designated federally authorized tax practitioner if they have questions or concerns in regards to the aforementioned topics.

About Five Stone Tax Advisers

Five Stone Tax Advisers has years of experience negotiating directly with the IRS to get the best possible outcome for you. Our International Tax Advisory and Compliance unit has a team of tax attorneys, certified public accountants and enrolled agents that form a single sourced point of contact that will provide services for all the legal, compliance and financial reconstruction aspects of offshore compliance cases.

FOUND THIS USEFUL ? SHARE WITH

by Five Stone Tax

Five Stone Tax is America’s trusted tax adviser, offering full-service tax solutions with the goal of making sure all of our clients pay the lowest amount of taxes legally possible. As the most effective tax representation company in America, our team consists of the best Property Tax Consultants, Tax Attorneys, Enrolled Agents, case managers, and administrators in the industry.

Subscribe to Our Blog!

Don’t miss out our filing tips & deadlines, global tax news and customer case studies

Give it a try—it only takes a click to unsubscribe.

have received several questions from current clients, prospective clients and other practitioners regarding the disclosure period for Offshore Voluntary Disclosure Program and Streamline filing compliance procedure.

have received several questions from current clients, prospective clients and other practitioners regarding the disclosure period for Offshore Voluntary Disclosure Program and Streamline filing compliance procedure.